The BFS problem nobody talks about

Business-for-self borrowers are the fastest-growing segment of the Canadian mortgage market. And they're the hardest files to close.

Not because the borrowers aren't creditworthy. Most BFS clients are successful business owners pulling real income from real businesses. The problem is proving it. A contractor earning $180,000 a year might show $68,000 on their T1 after legitimate deductions. A restaurant owner doing $400,000 in revenue might declare $55,000 in net income. The tax return tells one story. The bank account tells another.

That gap between declared income and actual cash flow? It lands squarely on the broker's desk.

What brokers actually do today

When a BFS deal comes in, the broker's job is to bridge that gap. Take the borrower's bank statements (12 to 24 months' worth, sometimes across multiple accounts) and build a case for what the borrower actually earns.

In practice, that means:

- Downloading every statement PDF from the borrower's bank portal

- Opening a spreadsheet and manually entering deposits and withdrawals, month by month

- Categorizing each transaction as business revenue, personal income, transfers between accounts, loan proceeds, or excluded items

- Identifying recurring deposits that qualify as stable income versus one-time inflows that don't

- Calculating a monthly average, then grossing it up by 15% to 25% depending on the lender's program

- Writing a summary letter explaining the income methodology to the underwriter

The reality of a typical BFS file

A clean file with one business account and straightforward deposits might take 3 hours. A messy one (multiple accounts, mixed personal and business transactions, foreign currency, Interac e-transfers with no memo) can take 6 to 8 hours. Some brokers have told us they've spent an entire weekend on a single BFS file.

And if the deal comes back with conditions? You open the spreadsheet again, re-do the analysis with the underwriter's adjustments, re-write the summary, and re-submit. That back-and-forth can add days to a deal that was supposed to close this week.

Why the manual process breaks down

The issue isn't that brokers lack skill. It's that the process doesn't scale.

Every BFS file is a custom job. There's no standard format for bank statement analysis across lenders. Different lenders want different gross-up percentages, different expense exclusions, different presentation formats. And requirements have tightened significantly. Many lenders now require 24 months of statements where they used to accept 12.

That means a broker doing 10 BFS deals a month could be spending 40 to 80 hours just on bank statement analysis. For context, that's a full-time job that produces no revenue on its own. It's the cost of doing the deal, not the deal itself.

And the errors compound. Misclassify a $3,000 monthly transfer between accounts as income and you've inflated the borrower's qualifying income by $36,000 a year. Miss an NSF fee and the underwriter flags the entire file for additional review. Manual work in a document-dense process (hundreds of transactions across dozens of pages) is inherently error-prone.

“I've been spending 8 hours on bank statement analysis. That's what got my attention.”

Mortgage broker

Alt lending specialist

What underwriters actually want

Here's what most brokers miss: underwriters aren't looking for a spreadsheet. They're looking for confidence.

They want to open a file and immediately understand:

- Where the income is coming from

- Whether the deposits are recurring and stable, or one-time and questionable

- How the gross-up was calculated and what methodology was used

- Whether there are any red flags (NSF fees, unexplained large deposits, gaps in activity)

- That each number in the summary can be traced back to a specific page and line in the source documents

When a file gives the underwriter that clarity, it moves. When it doesn't, it sits in the conditions pile. One broker told us that Scotia moves deals submitted with Purelend reports to the top of the pile, because the underwriter can see exactly where every dollar came from without having to cross-reference anything manually.

How Purelend changes the math

Purelend doesn't replace your judgment. It eliminates the manual labor that eats your day before you even get to use it.

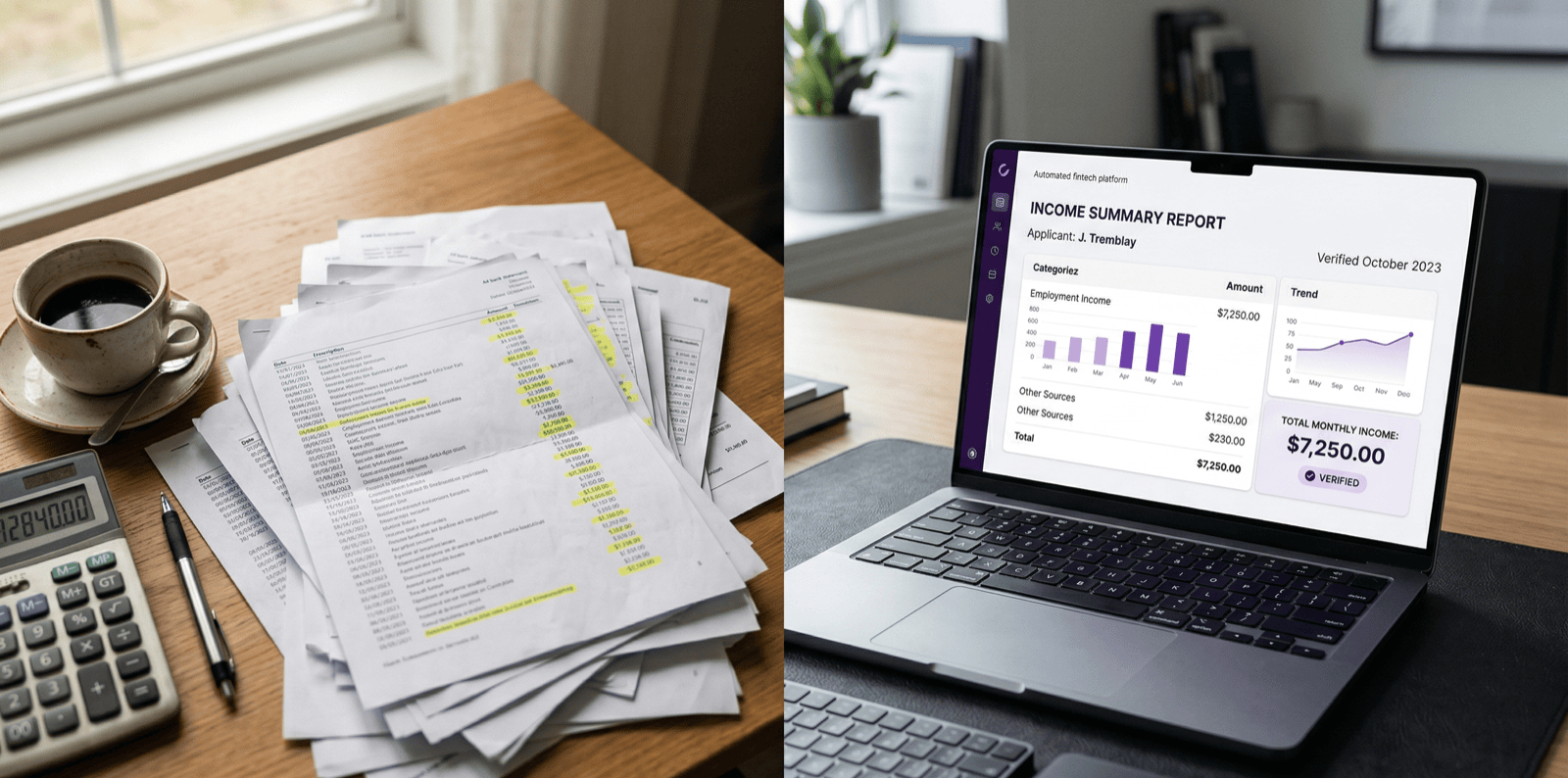

When you upload a BFS borrower's bank statements, Purelend reads every transaction across every account and automatically categorizes them: business revenue, personal deposits, inter-account transfers, expenses, excluded items. That baseline analysis takes about 3 minutes.

The Purelend process

- 1

Upload 12 months of bank statements (drag and drop, any format)

- 2

Purelend categorizes every transaction: revenue, personal expenses, business expenses, excluded credits

- 3

You review and adjust any categorizations in about 15 to 20 minutes (you stay in control)

- 4

Purelend generates a stated income report: net income baseline, gross-up calculation, NSF flags, all math shown

- 5

Export as an Excel spreadsheet with everything the lender needs. Include it in your submission package.

The report shows underwriters exactly how the income was calculated. No black box. Every transaction referenced by page and document.

Then you review. You're not building from scratch in a spreadsheet. You're looking at a pre-categorized breakdown and adjusting what doesn't match your knowledge of the client's business. Most brokers tell us that takes 15 to 20 minutes.

When you're done, Purelend generates a stated income report that includes:

- Monthly income breakdown with categorized transactions

- Net income baseline with the gross-up calculation applied

- NSF flags and any anomalies surfaced automatically

- Every figure referenced to a specific page and document in the source statements

- Export-ready Excel spreadsheet you can attach directly to your submission package

What used to be 4 to 8 hours of spreadsheet work becomes about 20 minutes of review. And the output is cleaner, more detailed, and more auditable than anything built by hand.

“This is more comprehensive than our manual spreadsheet process.”

Mortgage broker

Western Canada · Mix of A, B, and private deals

What this means for your business

Think about it in terms of deals. If you're spending 6 hours per BFS file on bank statement analysis, and you do 8 BFS deals a month, that's 48 hours. More than a full work week, just on income verification. Cut that to 20 minutes per file and you get 45 of those hours back.

Those aren't hypothetical hours. They're hours you can spend:

- Taking on more files

- Calling referral partners

- Actually following up on the 15 leads sitting in your pipeline

- Getting home before 9 PM on a Tuesday

And because the reports are consistently structured and auditable, you see fewer conditions come back from underwriters. Fewer conditions means faster closings. Faster closings mean happier clients and more referrals.

Brokers who specialize in BFS and alt lending tell us this is the highest-leverage tool they've adopted. Not because it does something they can't do themselves, but because it gives them back the time they were losing to the most tedious part of every deal.

The lender landscape is getting harder, not easier

Documentation requirements for self-employed borrowers have tightened significantly. Many lenders now require 24 months of bank statements where they used to accept 12. Some require CPA-prepared business financial statements on top of the standard T1 Generals and Notices of Assessment. Debt-to-income thresholds have dropped.

That means brokers are doing more work per file, not less. The volume of transactions to categorize has doubled. The documentation packages are thicker. The margin for error is slimmer.

This is exactly the environment where automation stops being a nice-to-have and becomes a competitive advantage. Brokers who can turn around a clean, auditable BFS package in under an hour will close deals that brokers still doing it by hand simply can't get to in time.