The objection we hear most

“I already have a system.”

We hear this on almost every demo call. And it makes sense. You've spent years building a workflow that works. Maybe you're on Finmo. Maybe Velocity or Expert or Scarlett. Maybe you've built your own process with spreadsheets, checklists, and a folder structure you could navigate in your sleep.

None of that needs to change. Purelend isn't replacing any of it. It's filling a gap that those tools were never designed to cover.

Your POS handles the application

Finmo, Velocity, Expert, Scarlett. All great at what they do: collecting borrower info, pulling credit, submitting to lenders, managing the pipeline. Keep using them.

What your POS wasn't built to do

Your POS is built for the application. It collects the borrower's information, runs the credit check, and submits the deal to the lender. That's the front end of the process, and those tools do it well.

But then the documents start coming in. Bank statements, pay stubs, T4s, Notices of Assessment, gift letters, property documents. And that's where things slow down. Because your POS doesn't verify income. It doesn't trace where a down payment came from. It doesn't flag inconsistencies or organize everything into a lender-ready package.

That work still falls on you. And if you're doing it manually, it looks something like this:

- Opening each document and cross-referencing it against the application

- Checking bank statements line by line for down payment sourcing

- Building spreadsheets to verify income across pay periods

- Writing deal notes to explain anything the underwriter might question

- Organizing the full package in the order the lender expects

That's hours per file. It's the most time-consuming part of the deal, and no POS tool on the market was designed to handle it.

Document collection is harder than it should be

Before you can even start reviewing documents, you need to get them from the borrower. And this is where the friction starts.

Most POS platforms offer some kind of document upload portal. But ask your borrowers how they feel about it. They need to create a new account. Remember another password. Navigate an interface that wasn't designed for them. Some portals enforce strict file size limits that reject scanned documents. Others ask the borrower to categorize each file before uploading (pay stub, T4, bank statement, gift letter) when the borrower barely knows what half of those are.

The result? Documents trickle in across email, text, and portal. Half the files are mislabeled. You spend time chasing what's missing and reorganizing what came in wrong. A typical mortgage file requires 10 to 15 documents, and processors managing 20 to 30 active loans can burn 2 to 3 hours per week just on follow-up.

It's a bad experience for the borrower and a waste of time for the broker. And it happens on every single deal.

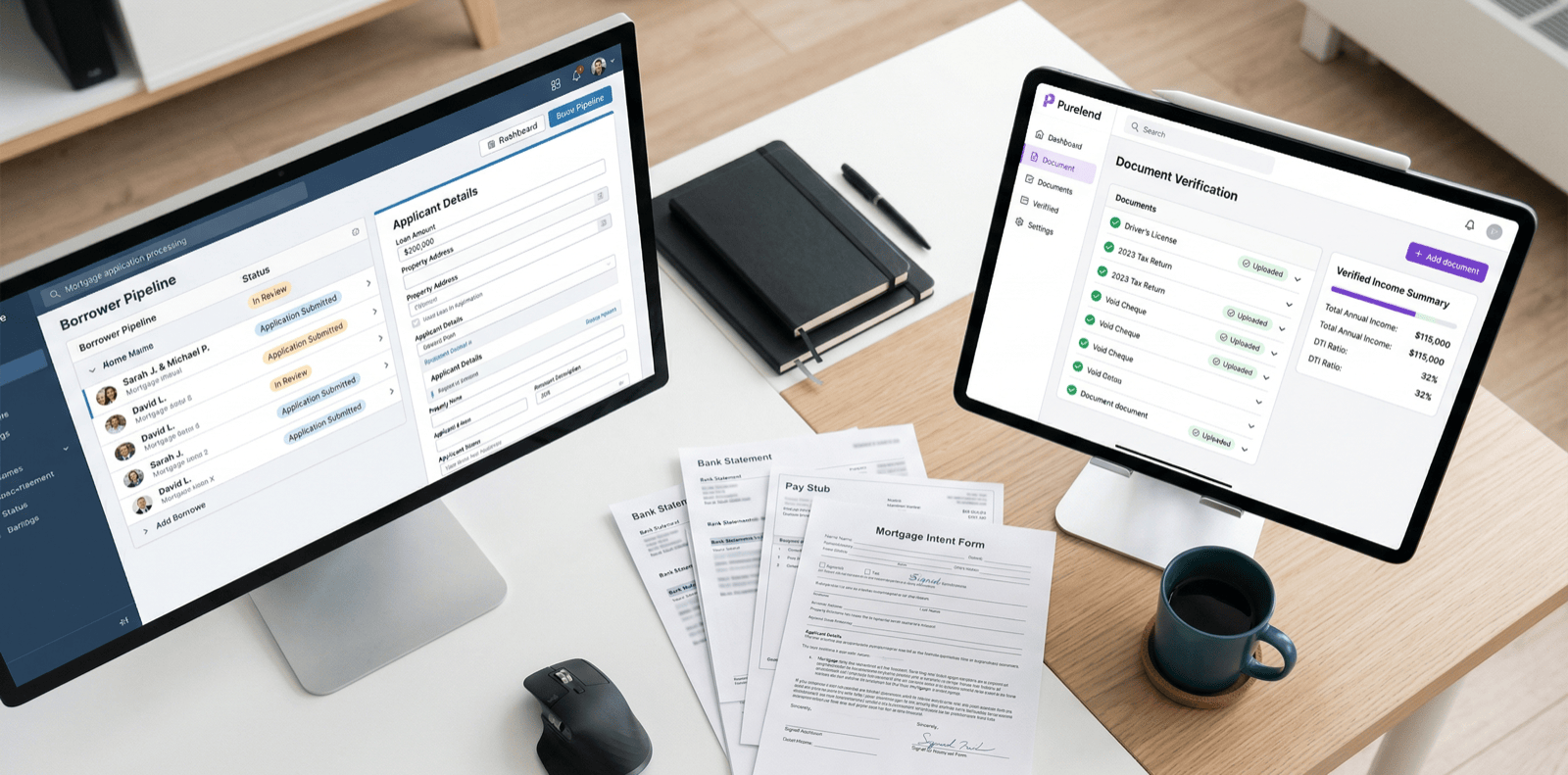

With Purelend, there's no new login for your clients. No account to create. No password to remember. You send a secure link with the checklist of required documents. Your client drags and drops their files. Purelend checks off the checklist automatically, converts everything, and organizes it for you.

What happens after the documents land

This is where Purelend does the work that used to eat your afternoon.

As soon as the borrower uploads their documents, Purelend starts processing. No manual trigger needed. It automatically:

- Identifies and categorizes each document (bank statement, pay stub, T4, NOA, and more)

- Extracts income data and verifies it against the application

- Traces down payment sources through bank statements, account by account

- Flags inconsistencies, NSF fees, and potential fraud indicators

- Generates a clean, structured report that summarizes everything the lender needs to see

You still review everything. You still make the judgment calls. But instead of spending hours building the analysis from scratch, you're spending minutes reviewing one that's already built.

What the underwriter actually sees

The quality of your submission package determines how fast your deal moves. A messy package with gaps and unexplained deposits gets sent back with conditions. A clean one with every figure sourced and referenced gets approved.

Purelend's reports give the underwriter exactly what they're looking for: where the income comes from, where the down payment came from, whether the numbers are consistent, and a clear reference back to the source documents for every figure. No guesswork. No back-and-forth.

One broker told us that Scotia moves deals submitted with Purelend reports to the top of the pile. When an underwriter can see exactly where every dollar came from without flipping through 50 pages of statements, the file just moves faster.

You submit a cleaner package

When underwriters can see exactly where every dollar came from, things move faster. Fewer conditions. Fewer delays. Faster closings.

The brokers who are already doing this

The brokers using Purelend aren't switching away from their POS. They're running both. Finmo or Velocity or Expert or Scarlett handles the application and submission. Purelend handles the documents that come in after.

The workflow stays the same. You collect borrower information in your POS the way you always have. When it's time to gather documents, you send the borrower a Purelend link instead of directing them to a portal they need to create an account for. The documents come in faster because the experience is easier. And when they land, you get a verified, organized package instead of a folder full of raw PDFs you need to review by hand.

That's it. No migration. No new pipeline to learn. No feature overlap. Just the piece that was missing.

Your tools are fine. Your process has a gap.

Finmo is great. Velocity is great. Expert and Scarlett are great. They solve real problems and most brokers couldn't operate without them.

But none of them were built to verify income from 12 months of bank statements. None of them trace a down payment through four accounts and three currencies. None of them generate a report that an underwriter can cross-reference against the source documents in seconds.

That's the gap. And the longer you fill it manually, the more deals you leave on the table because you're buried in document review instead of closing.